26 ديسمبر 2023

Author — Nick Korzhenevsky, senior analyst with AMarkets Company. The anchorman of a TV program “Economics. Day rates”.

Summary:

- Further dollar gains depend mainly on the U.S. GDP growth rate differentials over the rest of the DM world.

- EM markets can avoid a bloodbath, but the cycle pressure is getting more and more intense. China and the yuan pose the greatest risks.

- General volatility continues to rise as the ECB — world’s second largest liquidity supplier — prepares to hike interest rates and wind down QE.

- The political landscape should remain fairly quiet until September when Special Counsel Robert Mueller issues his report on the alleged Trump-Russia ties, and Italy’s new government delivers its first budget.

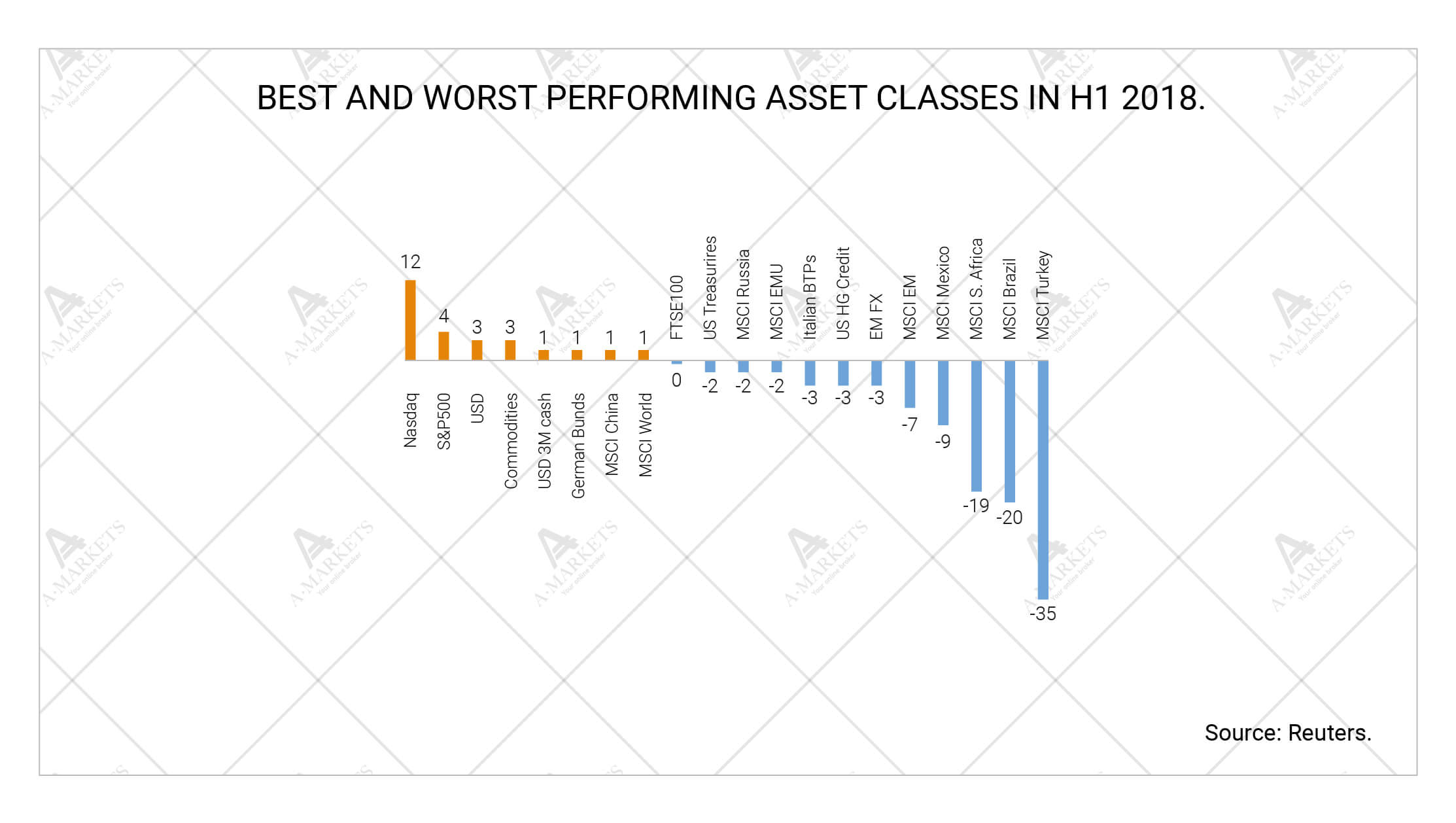

The first half of 2018 has come to a close, leaving us with what seems to be the payback for an unusually good 2017: risk-related assets have all moved down, while volatility is on the rise. New risks with the potential for serious systemic implications have emerged. Among them are the US-China trade war, the yuan’s weakness, and Italy’s troubled debt market. The former two are, of course, directly connected, and yet they manage to be a headache for market players in their own ways.

The ongoing trade wars remain of the primary concern. Tension between Washington and Beijing has been in the offing ever since Donald Trump won the presidency back in 2016, but investors just wouldn’t recognize that. At first, they were confident that the POTUS wouldn’t fulfill any of campaign promises, directing all of his efforts to fire back at Democrats and the FBI. That was until late 2017, when suddenly Trump’s tax reform became law, making it clear that things were getting serious.

Mr. Trump then explicitly stated his plans to impose tariffs on steel and aluminum imports from not only China, but also U.S. allies in Europe. That sounded like too big of a promise for investors, who, again, failed to price in an all-out trade war. They assumed Trump was only bluffing with his hawkish stance in attempt to make the opposing side settle for less. But things took an unexpected turn again: Trump met and shook hands with his fellow world leaders—he even called Canada’s Justin Trudeau his friend—only to proceed with the promised tariffs just weeks later.

What’s next? First, the U.S. has initiated a national security investigation into automotive imports under Section 232 of its trade law. These normally take about a year, but the Trump administration may want to complete the investigation before the mid-term election in November. We expect at least some sort of auto tariffs to be imposed, which will be another major blow to all of America’s trade partners, including Europe.

Second, the North American free-trade agreement (NAFTA) is still being negotiated, and Trump’s already proven that smiles and handshakes guarantee Trudeau nothing. We wouldn’t be surprised if Trump decides to withdraw the U.S. from the trade deal. Last but not least, the White House has hinted at possible investment restrictions. Now that’s a truly groundbreaking move which, if happens, will shake the markets harder than anything we’ve witnessed during this trade war so far.

Before we proceed to analyzing the implications of the above risks, let us point out something quite interesting. In September, Special Counsel Robert Mueller will announce the results his investigation on the alleged ties between the Trump campaign and Russia. Absence of substantial evidence—which would essentially rule Trump’s impeachment off the table—will serve as a green light for the White House to do whatever it wants. In fact, we are confident that all of the key market trends for Q4 2018 will be shaped by Muller’s report.

For investors, that means uncertainty, and uncertainty means volatility. Price fluctuations over the past few months have been very pronounced, unlike what we see throughout the 2017. And this is not changing anytime soon. But neither do we expect any significant directional moves in July or August, as these are likely to be triggered by politics.

The American dollar strengthened notably in Q2 on the back of the Fed’s hasty rate hike, as well as solid U.S. economic data. Trump’s aggressive trade policy appears to be having virtually no negative impact on the country’s real sector so far, which certainly gives him an edge over the rest of the world. Europe and China are already seeing a decline in economic growth, halting the talk of rate hikes. Furthermore, the ECB has announced that it will only exit QE in 2019, while the PBoC has eased its monetary policy and cut the reserve requirement ratio.

We still don’t think there’s anything out of the ordinary going on. Sure, the U.S. economy has proven to be relatively strong and hasn’t slowed down as much as it was expected to. On the contrary, growth rate in Europe and Asia has dipped. But as we have already mentioned in our previous reviews, economic growth is simply retreating from unsustainably high levels. The key question now is whether the rest of the world will be able to even up with the Uniter State. Our estimates suggest that the disbalance in H1 2018 was only temporary, and the growth in DM is likely to become even again.

We still don’t think there’s anything out of the ordinary going on. Sure, the U.S. economy has proven to be relatively strong and hasn’t slowed down as much as it was expected to. On the contrary, growth rate in Europe and Asia has dipped. But as we have already mentioned in our previous reviews, economic growth is simply retreating from unsustainably high levels. The key question now is whether the rest of the world will be able to even up with the Uniter State. Our estimates suggest that the disbalance in H1 2018 was only temporary, and the growth in DM is likely to become even again.

In that case, the dollar strength should also be short-lived. Most liquid currencies are likely to hover around current levels (exhibiting high intraday volatility) until September. And while there isn’t anything on the horizon to trigger major price moves, one should keep in mind the aforementioned Italian and Chinese risks.

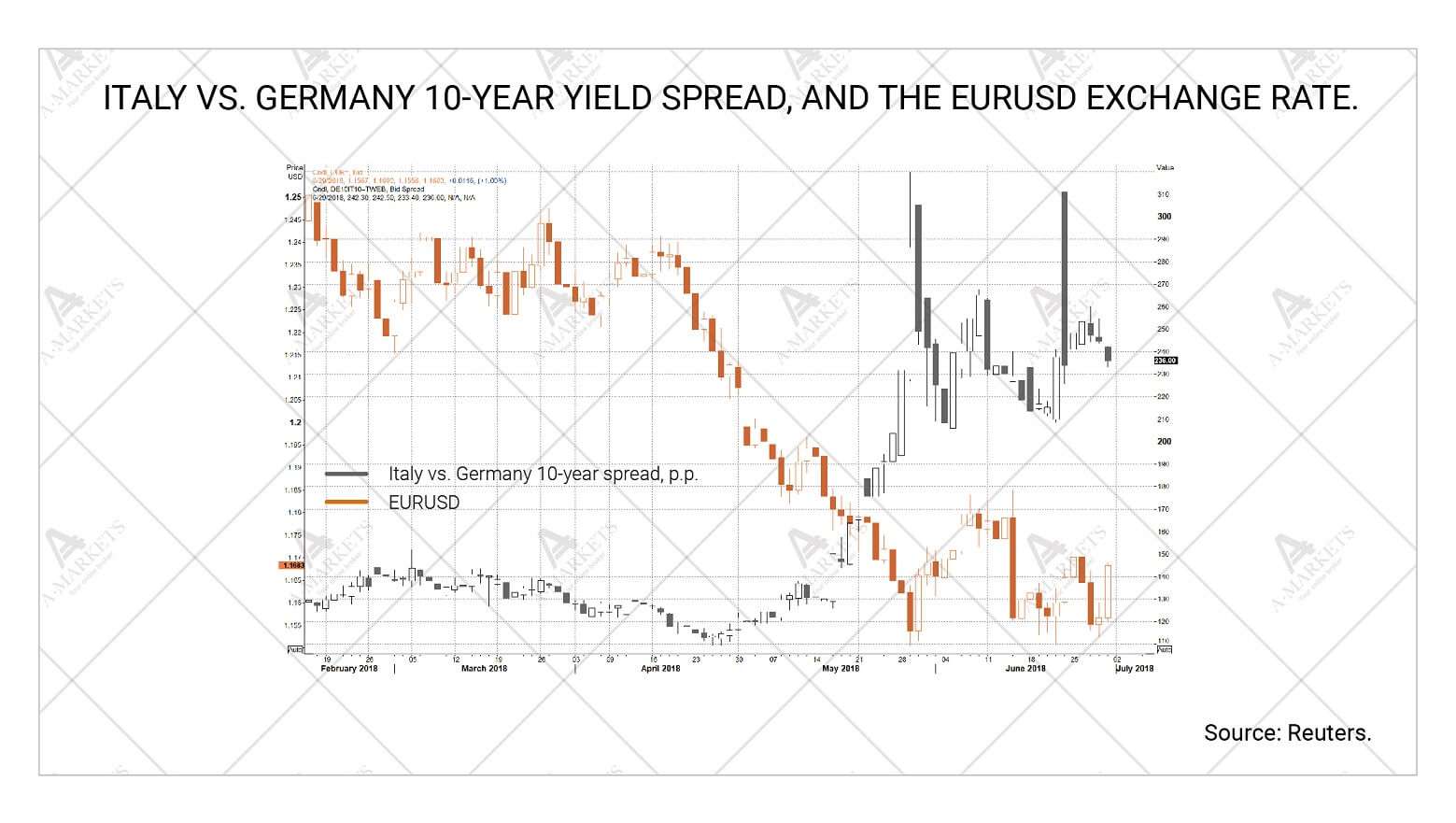

The Italian story was already covered in great detail. We don’t expect any fresh headlines out of Rome until September, when the new government is due to release its 2019 budget proposal. The pressure on Italy’s new cabinet is huge, and a badly-received budget plan can easily trigger another sell-off in the country’s sovereign debt market. Moreover, rating agencies are hinting that they are ready to review Italian creditworthiness, and could even go as far as downgrading it to junk. This is, of course, a nightmare scenario and it’s very unlikely that Rome will let it happen. At this point, however, we can’t rule out any outcome, and under this (again, unlikely) scenario dollar-euro parity wouldn’t be out of the picture.

The Italian story was already covered in great detail. We don’t expect any fresh headlines out of Rome until September, when the new government is due to release its 2019 budget proposal. The pressure on Italy’s new cabinet is huge, and a badly-received budget plan can easily trigger another sell-off in the country’s sovereign debt market. Moreover, rating agencies are hinting that they are ready to review Italian creditworthiness, and could even go as far as downgrading it to junk. This is, of course, a nightmare scenario and it’s very unlikely that Rome will let it happen. At this point, however, we can’t rule out any outcome, and under this (again, unlikely) scenario dollar-euro parity wouldn’t be out of the picture.

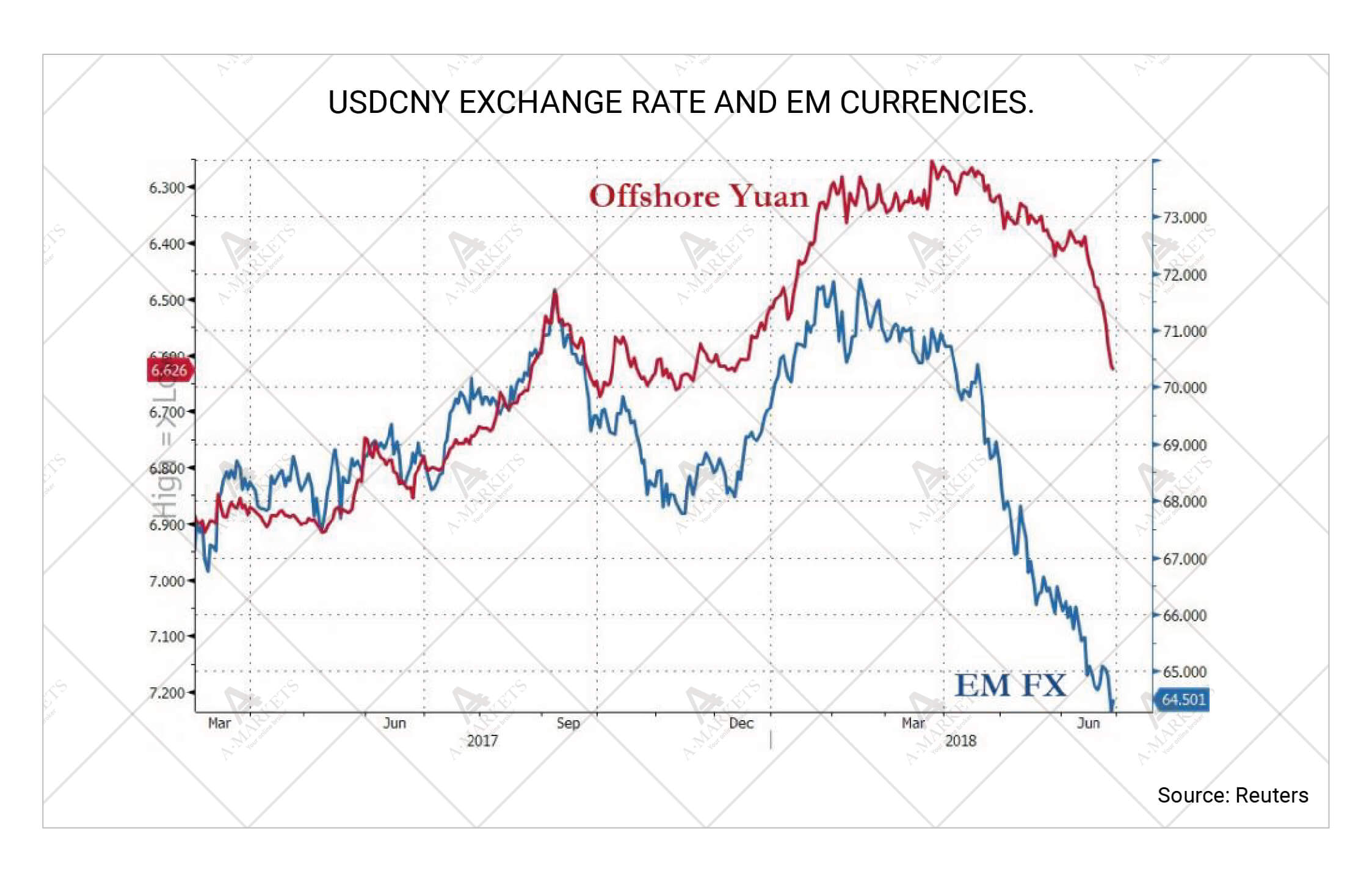

Now, the Chinese story poses way more tangible risks. The yuan is under pressure again as investors have finally come to the realization that the Trump administration can curb Chinese investments any day now. On top of that, the country is in a massive debt bubble that eventually will hit its limits too. China has successfully made it through the first wave of capital withdrawal from emerging markets, but it cost the government $1 trillion. Another episode of significant outflows would have serious implications, and some market players are already selling the renminbi, just in case.

That, in turn, puts pressure on the whole EM world. Plus, the Turkey and Argentina issues are still on the top of investors’ minds, which doesn’t help the situation either. This phenomenon is very clearly demonstrated by the rouble: even despite the rally in oil, the Russian currency continues to weaken. The same holds for the Norwegian krone, Mexican peso, and Canadian dollar (although the latter is not an EM-currency, so far it has been suffering from the trade wars just as much as they do). The entire EM-spectrum is likely to remain under pressure in the coming months, and if Trump does act on Chinese investments, emerging markets risk a major wave of sell-offs.

That, in turn, puts pressure on the whole EM world. Plus, the Turkey and Argentina issues are still on the top of investors’ minds, which doesn’t help the situation either. This phenomenon is very clearly demonstrated by the rouble: even despite the rally in oil, the Russian currency continues to weaken. The same holds for the Norwegian krone, Mexican peso, and Canadian dollar (although the latter is not an EM-currency, so far it has been suffering from the trade wars just as much as they do). The entire EM-spectrum is likely to remain under pressure in the coming months, and if Trump does act on Chinese investments, emerging markets risk a major wave of sell-offs.

Meanwhile, long-term investors should keep in mind that structurally the U.S. dollar is getting weaker. Not only are trade wars ominous for the balance of payments, but the tax reform in a rapidly extending economy will greatly deal the ability of the government to deal with the recession (and one is coming sooner or later). We are very cautious about buying the dollar against other G10 currencies, and view that type of positioning as extremely speculative. Going long USD against EM-currencies makes way more sense, but here, too, the degree of uncertainty is fairly high.

EURUSD: downtrend on hold, high-volatility consolidation ahead.

We buy EURUSD at 1.1505 targeting 1.183, stop-loss at 1.143, will then reverse our position targeting 1.119, stop-loss at 1.192.

The EUR/USD decline may not be finished just yet, but it has surely paused. Price activity suggests another leg down is eventually coming, with the targets lying just under the 1.12 mark. Entering short positions, however, seems premature for now as this is clearly a medium-term strategy. If you are feeling confident enough to jump in the trade, though, the 1.185-1.19 with a narrow stop-loss is your best bet.

The EUR/USD decline may not be finished just yet, but it has surely paused. Price activity suggests another leg down is eventually coming, with the targets lying just under the 1.12 mark. Entering short positions, however, seems premature for now as this is clearly a medium-term strategy. If you are feeling confident enough to jump in the trade, though, the 1.185-1.19 with a narrow stop-loss is your best bet.

The fundamental picture supports a similar viewpoint. As we have already pointed out, the next two months are unlikely to generate enough headlines to push the EUR/USD out of its current ranges (though, who knows what mess Trump’s twitter fingers might get us into tomorrow?) Over the short term, the euro will most likely hold between 1.15 and 1.18. Tactically, we view moves lower —which there will be plenty of thanks to the heightened volatility — as an opportunity for a speculative long.

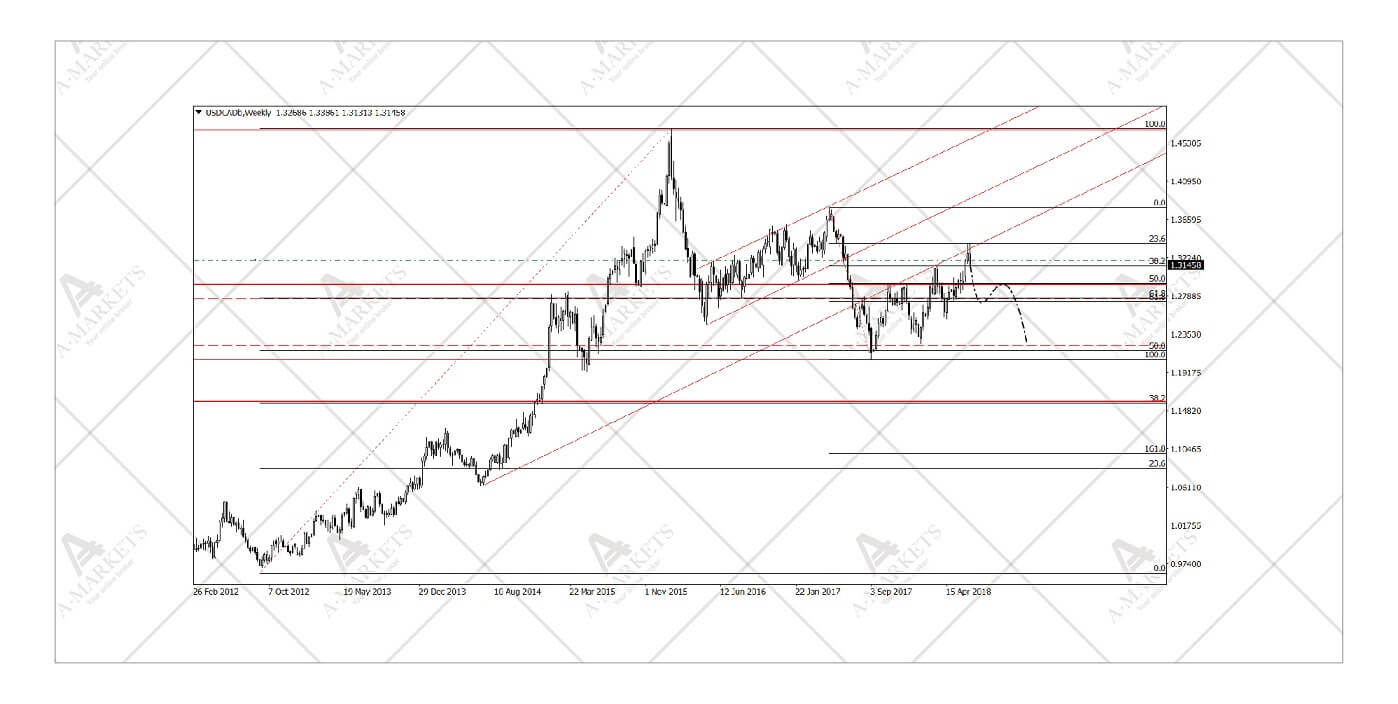

USDCAD: loonie now signficantly undervalued.

We sell USDCAD at 1.32 targeting 1.27/1.212/1.166, stop-loss at 1.3425.

The fact that the Canadian dollar is massively undervalued has been discussed many times. Even on the back of slower growth, the Bank of Canada is still headed for three rate hikes this year, meaning that it’s tightening its policy almost just as fast as the Fed. Oil prices remain trading at around $80 a barrel, while the loonie is currently priced for $45-50 a barrel.

The fact that the Canadian dollar is massively undervalued has been discussed many times. Even on the back of slower growth, the Bank of Canada is still headed for three rate hikes this year, meaning that it’s tightening its policy almost just as fast as the Fed. Oil prices remain trading at around $80 a barrel, while the loonie is currently priced for $45-50 a barrel.

The currency’s weakness over the past few months has been primarily driven by political factors, specifically Donald Trump’s trade fight with Canada. The American president still wants to either renegotiate NAFTA or drop out of it altogether. At this point, however, the markets know better than ignoring Trump’s promises and have largely discounted even the worst-case scenario. Negative surprises are now unlikely to exert serious pressure on the CAD, while positive ones should be able to give the currency a boost.

The technical picture looks favorable for a short position in the USDCAD as well. The cross tested the resistance level at 1.34 and then rapidly came back down. The next target comes in at 1.29, and then 1.274. We intend on closing 2/3 of the short at those levels. We do note, however, that the target 1.16 is still present on the long-term graph. Depending on how things go with NAFTA, as well as the USD dynamics in general, it could be smart to keep some of the position set to this ambitious aim.

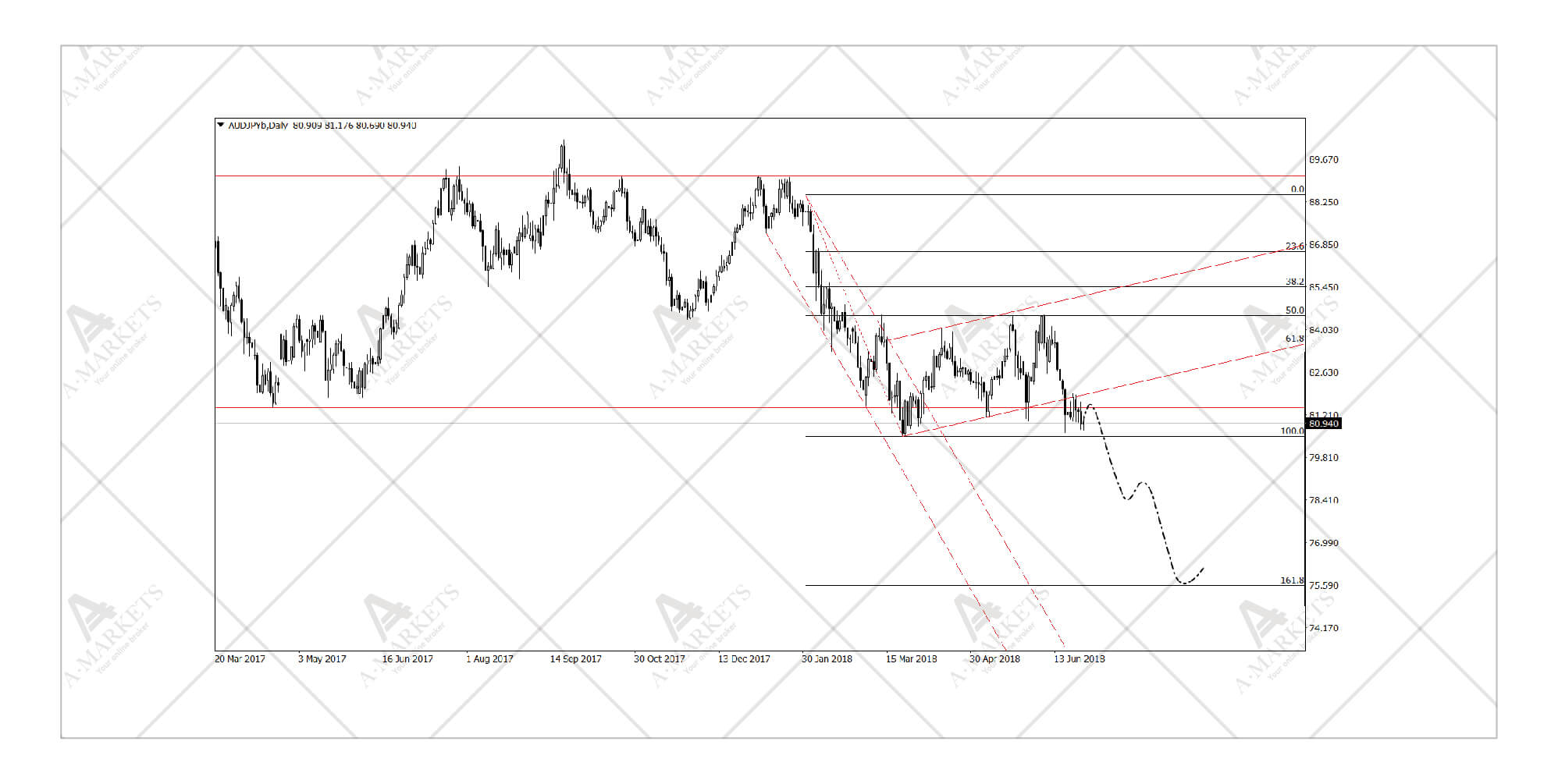

AUDJPY: entry points reached, targets still ahead.

We remain short AUDJPY targeting 75.7 and move stop-loss to the entry point at 84.3.

The AUD/JPY dynamics have been just as technical analysis had prescribed. June saw the pair correct to the 84.5 mark where we successfully opened a short position. Our target lies at just below 76, and there are no reasons to amend it. The Australian dollar is clearly the weakest link. First, the Reserve Bank of Australia found itself in a tight spot where it is unable to hike rates due to the housing market challenges. This means that as soon as other countries are normalizing their monetary policies, the AUD will be left an outsider.

Second, the Chinese yuan continues to weaken, hitting north of 6.6 per dollar in June. Given China is Australia’s top trade partner, any economic troubles in Beijing mean economic troubles in Canberra. Plus, the Japanese yen is on the rise as risk aversion intensifies. From the technical viewpoint, the cross failed to crack the psychological level of 80 and is now in a consolidation mode. We don’t expect any significant rebounds, however.

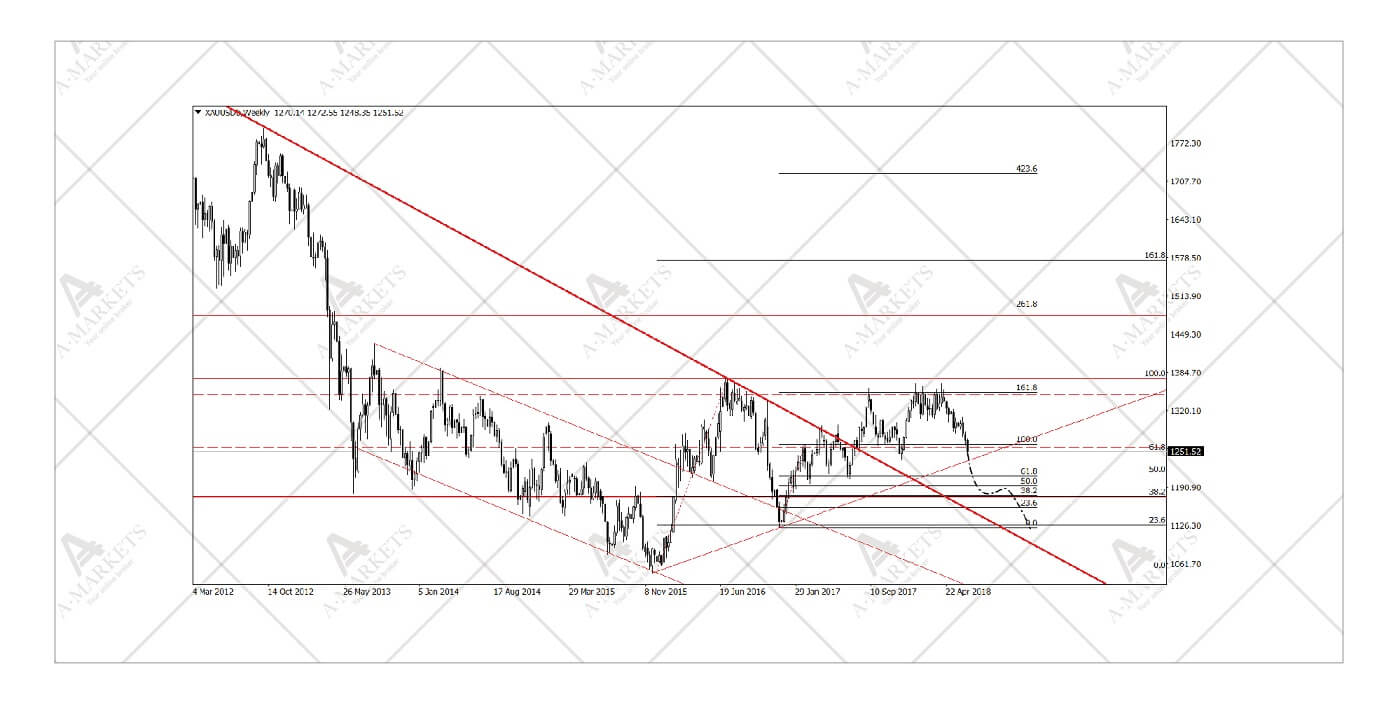

XAUUSD (Gold): gold unusually weak on muted dollar.

We sell XAUUSD at market targeting 1226/1130, stop-loss at 1292.

Perhaps the most important June story from the technical view point was gold breaking the long-term support line. There’s one last level at 1226-1236, but the prices are going down fast and on a very heavy volume. Unless the dollar weakens—which we don’t believe is likely—precious metals are at risk to further losses.

Technically, gold is on its way to an old target of just above $1,100 per troy ounce. Aside from the 1230 level, there is minor support in the 1190-1200 area. Oherwise nothing else is stopping the pair on its way south. This scenario is fundamentally supported by the normalization of monetary policies in the U.S. and other countries. Gold is not an interest-bearing asset, which makes it less attractive as rates go up.

We also remain long USDRUB and short S&P500.

Analytical materials and comments reflect only personal views of their authors and can’t be considered as trading advices. AMarkets is not responsible for losses as the result of analytical materials usage.